Current Mortgage Rates Today: Compare Today's Mortgage Rates and Stay Informed

Understanding today's mortgage rates is essential for anyone navigating the home financing process, whether you're a first-time homebuyer, current homeowner looking to refinance, or a seasoned real estate investor. At Mortgage Payment Calculator, we provide comprehensive insights into current mortgage rates, their historical trends, and expert rate forecasts to empower your decision-making. Compare offerings from various lenders including 30-year and 15-year fixed rate loans, FHA, VA, USDA, and jumbo mortgages. Stay informed about factors impacting rates such as credit scores, the Federal Reserve's monetary policy, and economic conditions to optimize your borrowing strategy effectively.

Compare Live Mortgage Rates From Lenders

Rates are updated regularly and may vary based on loan type, location, credit score, down payment, and fees. Click a lender in the table to view details and explore available options.

Tip: When comparing offers, look at both the interest rate and APR. APR includes certain fees and can make loans easier to compare.

Today’s Current Mortgage Rates Snapshot

Compare Mortgage Rates and Lender Quotes

Mortgage rates can change your payment, affordability, and total borrowing cost. Use this page to compare rate-driven loan options and review lenders that may fit your goals.

Brief Overview

Understanding mortgage rates is vital for homebuyers and homeowners to make informed financial decisions. Comparing rates for loans, such as 30-year or 15-year fixed, FHA, VA, and jumbo, can significantly impact borrowing costs. Factors like credit scores, down payments, and Federal Reserve policies influence these rates. By continuously monitoring trends, using tools like Mortgage Payment Calculator, and evaluating historical data, borrowers can identify optimal opportunities to purchase or refinance. This proactive approach helps maximize home affordability and achieve favorable mortgage terms.

Key Highlights

- Understand factors like credit score, down payment, and market conditions affecting borrowing costs.

- Compare rates for 30-year, 15-year fixed, FHA, VA, Jumbo, and refinancing options.

- Use tools like Mortgage Payment Calculator for lender comparisons and estimating monthly payments.

- Monitor rate trends and forecasts to identify opportunities for cost-effective borrowing.

- Evaluate credit scores' impact on the mortgage rates offered by lenders.

Understanding Today's Mortgage Rates

In the rapidly evolving world of real estate, understanding today's mortgage rates is crucial for both homebuyers and homeowners looking to maximize their financial decisions. Whether you're purchasing a new home, considering refinancing, or just keeping an eye on your investment, staying informed about today's mortgage rates can greatly impact your financial well-being. It's essential to compare rates daily because even a minor change in interest rates can affect the total cost of your mortgage over its lifetime. When examining current mortgage rates, consider multiple factors such as economic trends, Federal Reserve policies, and inflation. These elements can influence not only rates today but also beyond.

For those looking to better understand interest rates, it's important to familiarize yourself with different types such as 30-year fixed, 15-year fixed, FHA, VA, and Jumbo loans. Each type of loan will have unique interest rate considerations, so learning about these can provide deeper insight into securing the best rate possible. Rates today can be swayed by a borrower's credit score, debt-to-income ratio, and the size of your down payment. Better scores and larger down payments generally lead to more favorable rates.

Monitoring rate trends can help you make well-informed decisions when locking in a rate. Historical data can often give clues about where interest rates might be heading, prompting smart moves in planning home purchases or refinancing endeavors. By actively comparing interest rates, you can identify beneficial opportunities tailored to your financial situation. Using online tools, such as those provided by Mortgage Payment Calculator, allows you to easily evaluate multiple loan options and stay abreast of daily changes. In conclusion, regularly reviewing current mortgage rates equips you to make smarter borrowing choices, ultimately enhancing your home affordability and financial security.

Factors Influencing Rates Today

In the dynamic world of home financing, understanding factors influencing rates today is essential for borrowers aiming to stay informed and make sound decisions. Current mortgage rates fluctuate due to several key factors, each playing a significant role in determining the interest rate a borrower might receive. The overall economic landscape, including inflation rates, Federal Reserve policies, and bond market performance, heavily influences today's interest rates. When inflation rises, interest rates often follow suit to ensure lenders achieve a real return on their investments.

Credit scores are paramount in influencing current mortgage rates. Borrowers with higher credit scores often secure better interest rates, as a strong credit history signifies lower risk to lenders. Therefore, maintaining a good credit profile is beneficial when shopping for competitive rates today. Other crucial aspects include the loan amount and the size of the down payment. Larger down payments can lead to more favorable rates by reducing the loan-to-value ratio and mitigating lender risk.

The type of loan product you're utilizing - whether a 30-year fixed, 15-year fixed, FHA, VA, or jumbo loan - also dictates the interest rate you'll encounter. Each loan type has specific characteristics that influence both the rate and its suitability for different borrower profiles. Additionally, individual lender policies and the competitive landscape among financial institutions can further affect rates. Comparing current mortgage rates across lenders can help identify potential variations to leverage when negotiating.

Your debt-to-income ratio is another factor. A lower ratio indicates greater financial stability and could result in better rates today. Additionally, external factors such as geopolitical developments and shifts in investor sentiment can also ripple through to influence rates. By understanding these numerous elements, homebuyers and refinance borrowers can better navigate the challenges of securing favorable interest rates. Leveraging online tools for rate comparisons and monitoring these factors can empower better decision-making and secure cost-effective borrowing solutions.

How Credit Scores Impact Mortgage Rates

When it comes to securing a mortgage, your credit score plays a pivotal role in determining the mortgage rates you’re offered. Higher credit scores typically translate to more favorable rate mortgage terms, while lower scores can result in higher mortgage rates and increased borrowing costs. This difference in interest rate can have a significant impact on the overall affordability of your mortgage. With today’s competitive market, understanding how your financial standing affects the interest rate is crucial.

Your credit score is calculated based on your credit history, which includes your payment track record, the amount of debt you carry, and the length of your credit history. Lenders use this score to assess your reliability in repaying a loan, which heavily influences the rate mortgage offered to you. A higher credit score usually qualifies you for lower mortgage rates, translating to lower monthly payments and less interest paid over the life of the loan.

Conversely, a lower credit score can lead to higher interest rate charges, thereby increasing monthly mortgage payments and the total amount of interest rate paid over time. It’s essential to regularly monitor your credit and engage in practices such as timely payments and reducing your debt-to-income ratio to improve your credit standing. As you evaluate today’s mortgage rates and look to compare various lender offerings, paying attention to how your credit score impacts these rates is vital.

Factors such as Federal Reserve policy and bond market movements also influence current mortgage rates, but your personal credit standing remains one of the most significant factors in rate determination. By understanding how your credit history affects the mortgage you can secure, and staying informed about rate trends, you’ll be better positioned to obtain a favorable interest rate that suits your financial goals.

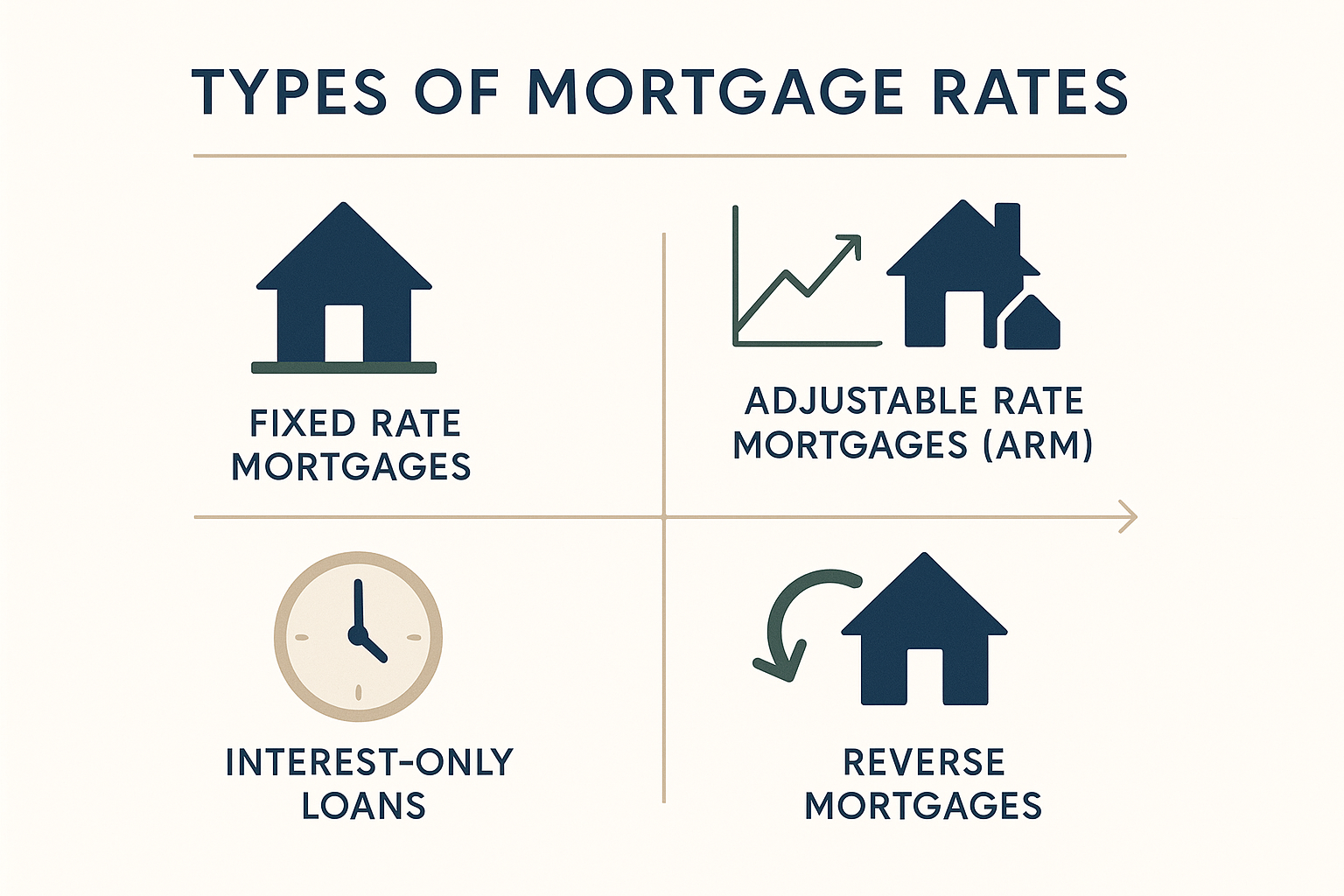

Types of Mortgage Rates Available

When navigating the complex landscape of mortgage rates, it's essential to understand the various mortgage types available to suit your financial goals. Among the most recognized are the 30-year fixed and 15-year fixed mortgage rates. These provide stability in monthly payments over their respective terms, appealing to borrowers planning long-term home occupancy. The 30-year fixed mortgage offers predictable payments spread over 30 years, whereas the 15-year fixed mortgage allows for faster equity build-up with generally lower interest but higher monthly payments over 15 years. Additionally, there's the FHA mortgage, designed to make home ownership more accessible with lenient credit requirements and lower down payments. VA mortgage rates cater to veterans and active-duty military members, offering benefits like no down payment and competitive interest rates. If you consider purchasing a high-value property, jumbo mortgage rates come into play, exceeding the conventional loan limits and potentially carrying higher interest costs due to increased risk to lenders. Refinancing your existing mortgage could also lower your rate mortgage, giving access to improved terms by replacing your old mortgage with a new one at current mortgage rates. Understanding these rate types will help you evaluate different mortgage rates based on factors like loan length, borrower qualifications, and property price. Constantly reviewing mortgage rates is crucial, especially considering how dynamic they are, influenced by market trends, lender competition, and economic conditions. Whether purchasing a new home or considering options for an existing mortgage, you should explore all available rates to ensure you're making informed decisions that align with your financial circumstances. Each rate mortgage type offers distinct features; evaluating them will significantly contribute to achieving your home financing objectives. With numerous mortgage rates and mortgage products to choose from, your path to securing the ideal mortgage becomes clearer when you completely grasp the available options. Use our Mortgage Payment Calculator to explore rate scenarios today.

30-Year Fixed vs. 15-Year Fixed: Which Is Right for You?

Deciding between a 30-year fixed and a 15-year fixed mortgage is a crucial consideration for prospective homeowners and current property owners looking to refinance. Both loan types offer distinct advantages, influencing your monthly payments and financial outcomes over the life of the mortgage. A 30-year fixed mortgage typically results in a lower monthly payment, allowing you to stretch your investment over more years, affording you the ability to allocate funds elsewhere or manage your monthly binding commitments comfortably. The fixed interest rate ensures that your monthly payment remains consistent, providing stability to your financial planning over the years. On the other hand, a 15-year fixed mortgage demands higher monthly payments due to the shorter loan term, meaning you'll pay off your mortgage faster and build home equity more quickly. This fixed-term option can also result in substantial interest savings over the years, as the total interest paid is lower compared to a 30-year fixed mortgage. Understanding your financial goals and current market conditions, including today's mortgage rates, is crucial in choosing between these fixed-rate options. Exploring factors like credit score and down payment is essential, as they significantly influence the rates you're offered. Utilizing resources like Mortgage Payment Calculator, you can estimate monthly payments and compare how different scenarios impact your financial situation through time. Whether you prioritize minimizing monthly payments with the extended nature of a 30-year fixed loan or maximizing interest savings over fewer years with a 15-year fixed loan, understanding each option ensures you align your mortgage decision to your financial strategy effectively.

Exploring FHA, VA, and Jumbo Loan Options

Choosing between FHA, VA, and Jumbo loans can significantly affect your rate and monthly payment calculations. Each loan type offers unique advantages, but understanding them fully ensures you secure the best possible rate and the most affordable monthly payment tailored to your financial circumstances.

An FHA loan is often popular among first-time homebuyers because it offers competitive rates and requires a lower down payment than conventional loans. However, FHA loans necessitate mortgage insurance, which can impact overall payments. It's crucial to evaluate the cost of insurance when considering your monthly payment and determine if the benefits outweigh the additional insurance costs. An FHA loan's rate might be influenced by your credit score and prevailing market conditions, which also affect the APR you'll ultimately pay.

On the other hand, VA loans provide an enticing alternative for eligible veterans, offering no down payment option and no mortgage insurance requirement. This can lead to significant savings in monthly payments and APR. Keep in mind that the VA funding fee, assessed in place of traditional mortgage insurance, may vary based on down payment and service history, affecting your overall borrowing costs and monthly payment amounts.

Lastly, a Jumbo loan might be necessary if you're buying a high-value home exceeding conventional loan limits. These loans often command higher rates due to their size and lenders' increased risk. Borrowers should anticipate a more stringent qualifying process, impacting their rate and required down payment. Comparing offers from various lenders can reveal differences in rates, APR, and overall cost, highlighting opportunities for optimal rates and monthly payments.

When exploring these loan options, staying vigilant of current rates and monitoring rate trends can help ensure that the deal you secure aligns with your financial goals. Utilize online tools such as those available at Mortgage Payment Calculator to compare offers, understand insurance necessities, and make informed decisions tailored to your specific rate and monthly payment needs.

Comparing Current Mortgage Rates

When it comes to making informed decisions on a mortgage, it’s vital to compare today’s mortgage rates and understand current mortgage rates to ensure you’re securing the most favorable terms. These rate mortgage comparisons play a crucial role in determining your borrowing costs and long-term financial commitment. By regularly assessing mortgage rates available today, potential homebuyers and existing homeowners can better navigate a fluctuating market and take advantage of opportunities to lock in low rates.

Every rate can substantially impact monthly payments and total interest paid over the loan's life. Hence, knowing the differences in mortgage rates is crucial. Whether you’re contemplating a conventional mortgage or evaluating FHA, VA, or Jumbo loan options, understanding each rate, along with the associated terms and conditions, is necessary before choosing a lender.

Today's mortgage rates fluctuate based on numerous factors, and acting on this knowledge empowers buyers and homeowners to maximize their investment. Depending on personal financial nuances such as credit score, down payment, and loan type, the rate mortgage that best suits will vary. The Federal Reserve's policies and broader economic indicators also directly affect current mortgage rates, meaning a proactive approach is essential for finding an optimal rate.

Comparing rates today not only involves reviewing the rate but also understanding the hidden intricacies in mortgage terms. Online tools like the Mortgage Payment Calculator provide a reliable platform to assess rate variations, allowing you to simulate different scenarios and their financial impact, ensuring you make educated decisions. Whether opting for a 30-year fixed rate or a 15-year fixed rate mortgage, evaluating these rates today opens up possibilities for cost-effective refinancing and investment strategies.

By staying informed and comparing current mortgage rates, you can safeguard against the volatile nature of the mortgage markets and work towards a brighter financial future.

How to Shop for the Best Rates

When it comes to finding the best mortgage rates, strategic shopping and using reliable resources can make a significant difference in securing favorable home loans. Start by visiting platforms like Mortgage Payment Calculator, which provide comprehensive rate comparisons and current mortgage rate trends for a variety of loan options. By leveraging a calculator, you can estimate your monthly payments and understand how different mortgage rates and terms affect your finances. It’s crucial to compare offers from various lenders, including 30-year fixed rates, 15-year fixed rates, and specialized loans like FHA, VA, and jumbo options. Understanding the factors that influence rates, such as market conditions and personal credit history, will empower you in negotiating the best rate possible.

Begin by researching today's mortgage rates thoroughly. Pay attention to promotional rates in market advertisements, but also verify claims using a reliable rate calculator. Look beyond the surface and inquire about potential rate changes as market conditions fluctuate. Since different lenders offer varying rates, utilizing a rate calculator helps you identify and capitalize on the most competitive offers in real time. Additionally, consider pre-approval processes that not only clarify how much you can borrow but also potentially secure a rate lock, shielding you from sudden rate increases as you shop for your home.

Remember that borrower-specific factors like your credit score significantly impact the mortgage rates you're offered. Improving your credit score before applying can decrease your rate, so regularly check your credit report to ensure accuracy. Be attentive to debt-to-income ratios and make substantial down payments to improve your overall loan profile. Maximize your home affordability by remaining informed about ongoing rate updates and forecasts. By taking these steps and using tools such as the Mortgage Payment Calculator while shopping for rates, you set yourself up for success, obtaining the best possible terms and rates tailored to your financial situation.

Using Online Tools for Rate Comparisons

In today’s fast-paced real estate market, staying informed and making precise decisions is crucial for anyone involved in the mortgage process. A major aspect of this process is using online tools for rate comparisons, ensuring you’re getting the most affordable rates possible. Rate tools, such as calculators, can help you assess daily mortgage fluctuations and secure average mortgage rates that fit your financial situation. Online tools streamline the process of comparison, providing a broad overview of loan options available. By integrating various calculators and comparison tools, borrowers can easily conduct thorough rate comparisons to assess rate averages across lenders. This approach empowers users to make informed decisions by comparing current rates accurately and efficiently.

Insurance is another element these online tools can accommodate, offering insights into how it impacts loan options and affordability. Borrowers often overlook insurance, yet it plays a significant role in monthly payments and overall loan costs. With the right comparison tools, it’s possible to factor in insurance costs, lending insight into true affordability. Tools have revolutionized how users can evaluate current mortgage rates, offering personalized scenarios accounting for various financial inputs.

Keeping abreast of changing rates is vital, and online tools allow for real-time rate comparisons. This allows potential borrowers to seize opportunities presented by advantageous rate shifts. Effective use of online tools ensures that both new homebuyers and those seeking to refinance can make educated decisions based on accurate, up-to-date information. They allow for a transparent view of rate dynamics, highlighting competitive offers that may otherwise go unnoticed. The constant evolution in web technologies continues to enhance the capacity of these calculators, making them indispensable in modern mortgage rate evaluation. Exploring various online rate tools establishes a solid foundation for identifying the best loan options, paving the way for financial success and secure investments.

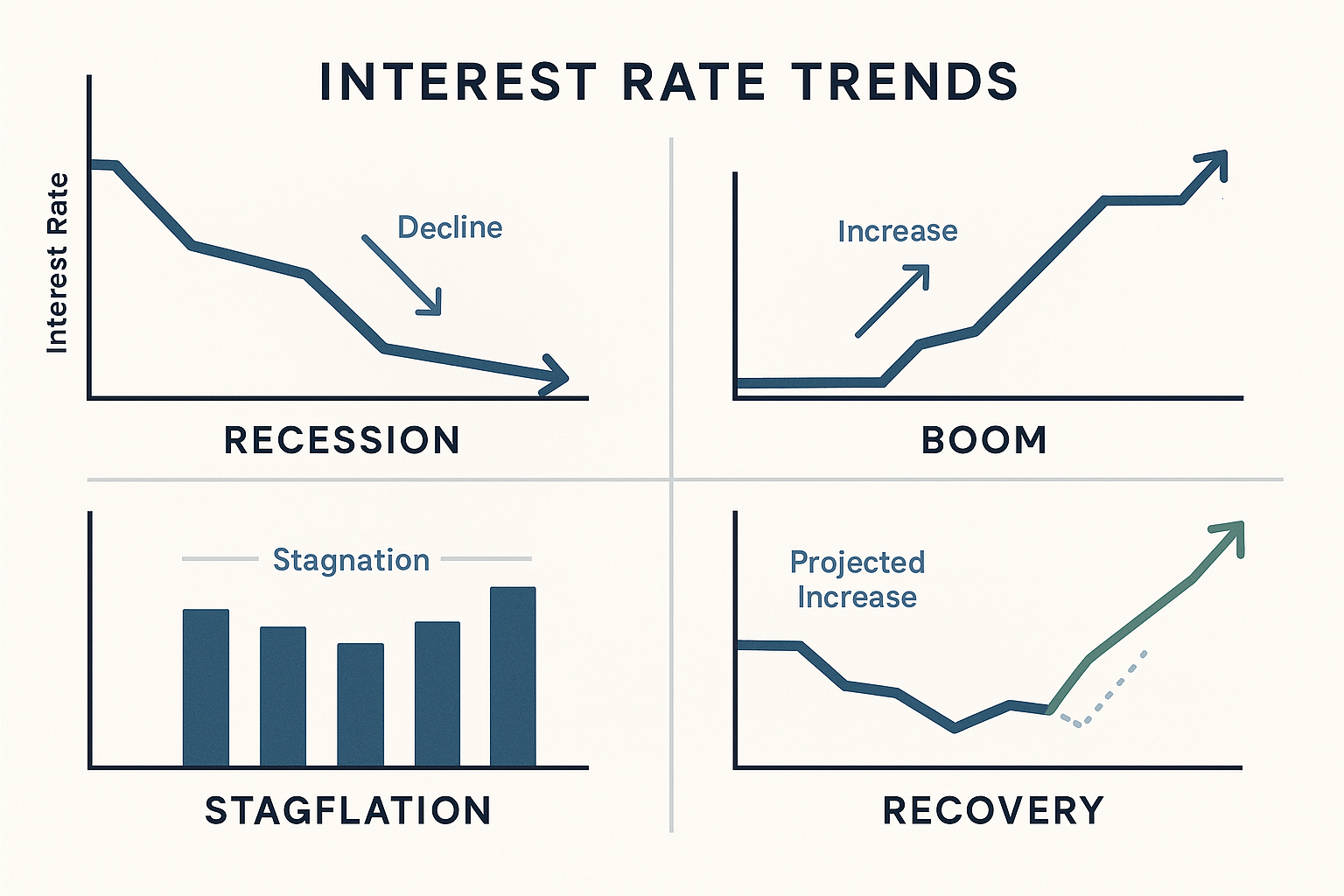

Evaluating Interest Rate Trends

When it comes to evaluating interest rate trends, understanding the nuances of mortgage rates can greatly impact your financial decisions. Mortgage rates today are shaped by various factors, and assessing these trends helps borrowers make well-informed choices. Interest rate insights can reveal how historical interest rate patterns and current market dynamics affect rates today. As mortgage rates fluctuate, staying updated on interest rate trends allows you to navigate the ever-changing lending landscape.

One crucial aspect of evaluating interest rate trends is understanding the factors that influence mortgage rates. Elements such as inflation, economic indicators, and Federal Reserve policies contribute significantly to today's rates. Not only do these factors impact current mortgage rates, but they also provide essential clues for forecasting future mortgage rate movements. By analyzing these influences, borrowers are better equipped to anticipate changes and adapt their strategies accordingly.

Monitoring rate trends is pivotal for homebuyers looking to secure favorable loans. Comparison shopping becomes more effective when you're aware of how interest rates compare across different loan types, such as 30-year fixed, 15-year fixed, FHA, VA, and jumbo loan rates. This knowledge allows borrowers to capitalize on optimal lending scenarios, potentially saving thousands over the life of a loan. Additionally, understanding historical interest rate patterns can provide valuable context, illuminating how past events have shaped mortgage rates today.

Evaluating interest rate trends also offers insights into refinancing opportunities. Whether your goal is to reduce monthly payments or shorten your loan term, keeping an eye on interest rate movements ensures you can make timely refinancing decisions. By leveraging resources like the Mortgage Payment Calculator, you can easily estimate how different rates affect your payments, thereby maximizing your financial advantage.

In summary, evaluating interest rate trends is essential for anyone involved in real estate transactions. Identifying shifts in mortgage rates today empowers borrowers to make strategic decisions, while remaining informed on rate trends supports sustainable financial planning. Embrace the dynamic nature of the market and stay proactive in your approach to achieving homeownership goals.

| Key Component | Influencing Factors | Potential Impact | Strategic Insights |

|---|---|---|---|

| Economic Indicators | GDP growth, employment rates, and inflation. | Strong GDP and employment can lead to rate hikes; inflation affects purchasing power. | Monitor economic reports to time borrowing effectively; consider fixed-rate options in rising environments. |

| Federal Reserve Policies | Monetary policy and benchmark interest rates set by the Federal Reserve. | Fed policy changes can directly alter mortgage rates. | Stay informed on Fed meetings and statements; adjust refinance strategies accordingly. |

| Market Sentiment | Investor confidence and stock market trends. | Positive sentiment can drive investment flows, influencing interest rates. | Evaluate market behavior; consider locking rates during times of uncertainty. |

| Global Events | Geopolitical stability and international economic development. | Global disruptions can lead to fluctuating interest rates due to risk adjustments. | Adapt to changing conditions by diversifying loan portfolio risks. |

This table encapsulates critical elements for understanding and forecasting interest rate trends, enabling strategic decision-making in the mortgage market.

Historical Interest Rate Patterns

Understanding historical interest rate patterns is crucial for anyone looking to navigate the mortgage market effectively. Past interest rate patterns offer a wealth of data that can provide insights into interest rate trends and how they can impact borrowing costs. By studying these patterns, borrowers can better predict potential shifts and make more informed decisions. Historical patterns show us how external factors like economic downturns, inflation, and Federal Reserve policies have influenced rate patterns over time.

Evaluating patterns in interest rates also helps in understanding cyclical movements. By analyzing historical interest rate fluctuations, one can observe recurring trends that may suggest future directions in the interest rate environment. This understanding is essential for borrowers who aim to lock in favorable terms before any significant rate hikes occur. Utilization of historical data allows potential homebuyers and refinancers to anticipate possible interest rate changes.

Examining past patterns in interest rate trends empowers individuals to gauge future possibilities. Historical analysis of rate trends provides a benchmark for what borrowers might expect and prepares them to adapt their strategies accordingly. A continuous assessment of trends ensures that borrowers remain informed, helping them decide the best times to purchase or refinance.

Gaining insight into historical interest rate fluctuations aids in forecasting future possibilities. While no one can predict interest rate shifts with absolute certainty, by closely monitoring historical rate patterns, individuals place themselves in a stronger position to identify opportunities and threats. Staying updated on these rate movements enables borrowers to make educated strides toward securing their ideal mortgage terms.

Interpreting historical interest rate patterns gives clarity into the evolving nature of the mortgage market. With historical reference points, borrowers can understand past market reactions to certain events, allowing them to better prepare for potential rate environment changes. This knowledge is indispensable for financial planning in home buying or refinancing decisions.

Based on the discussion of historical interest rate patterns, here are some practical steps borrowers can take to apply this knowledge:

- Regularly review historical interest rate trends to identify potential future shifts.

- Stay informed about Federal Reserve policy decisions that impact interest rates.

- Monitor inflation rates as a potential indicator of upcoming interest rate changes.

- Analyze economic indicators for signs of cyclical movements in interest rates.

- Consider fixed-rate mortgages to mitigate the risk of fluctuating interest rates.

- Use historical data to time your mortgage application strategically before anticipated rate hikes.

- Stay updated with financial news and expert predictions on interest rates.

By implementing these strategies, borrowers can better navigate the complexities of the mortgage market and secure favorable terms.

Forecasting Future Mortgage Rate Movements

Forecasting future mortgage rate movements is crucial for homebuyers, homeowners, and investors looking to make informed decisions. Accurately predicting the future mortgage rate landscape involves understanding the interplay of several economic factors. These include inflation, Federal Reserve policies, and broader financial market conditions. When forecasting future rates, it's essential to analyze trends, including interest rate movements influenced by domestic and global economic indicators. Future mortgage rate forecasts help potential borrowers grasp the implications on their financial commitments. Changes in interest rate movements can significantly impact mortgage affordability and the overall cost of financing a home.

As individuals strive to forecast future rates, they must pay attention to both short-term and long-term mortgage rate movements. These movements might be affected by shifts in the economy, such as employment levels, GDP growth, and geopolitical events, which can cause fluctuations in lenders' rate offerings. Mortgage Payment Calculator provides insights into these trends by tracking historical data and analyzing current market conditions. This enables users to better understand forecasting interest tendencies and make decisions that align with their financial goals.

By continuously monitoring rate trends, potential homebuyers and refinance borrowers can identify optimal times to engage lenders and lock in favorable rates. Engaging in forecasting future mortgage rate movements allows for a proactive approach, helping mitigate risks associated with unexpected rate hikes or market volatility. Additionally, such forecasting efforts empower individuals to adapt to future movements, ensuring their borrowing strategies remain resilient amidst changing economic climates.

Ultimately, staying informed about forecasting interest rate movements is an integral part of a sound financial plan. Understanding these patterns permits individuals to secure advantageous borrowing terms. Whether you're a first-time buyer, a seasoned homeowner, or a real estate investor seeking to capitalize on market conditions, forecasting future mortgage rate movements provides the knowledge needed to navigate the complexities of home financing with confidence.

Maximizing Home Affordability with Smart Borrowing

Maximizing home affordability is crucial for any aspiring homeowner, and understanding home affordability trends is the first step towards making informed decisions. When you're planning to buy a home, smart borrowing plays an essential role in ensuring that you don't overspend on monthly payments. Mortgage rates are a key factor, as they dictate the overall cost of borrowing. By staying informed about rate mortgage options and average mortgage rates, you can find favorable terms that align with your financial goals. Today, more than ever, it's vital to understand the impact of various borrowing options to enhance overall affordability. Whether you're looking at a 30-year fixed rate mortgage or exploring the advantages of a shorter term, knowing the average mortgage rates helps you gauge your monthly payment accurately. Additionally, considering how different factors like credit scores and down payments affect mortgage rates can greatly impact home affordability. Engaging in smart borrowing strategies involves comparing different mortgage rates and rate averages available in the market continuously. By doing so, you can ensure that you secure the best possible deal, making the most of your home affordability with smart financial planning. Interestingly, the impact of borrowing costs can be influenced by external factors like inflation and Federal Reserve policies, making it important for homebuyers to monitor trends and forecast movements to capitalize on opportunities effectively. With the right approach, maximizing home affordability can lead to significant financial savings in the long run. Monthly payments shouldn't be a burden but rather a manageable expense that suits your financial plan. Utilize available online tools for mortgage rate comparisons and ensure you're well-equipped to make sound borrowing decisions. With the right knowledge and strategy, you can exploit the benefits of smart borrowing and home affordability, making your homeownership journey smoother and more cost-effective.

Staying informed about current mortgage rates is essential for making sound financial decisions. By comparing today's mortgage rates with those of previous periods and projections for future trends, borrowers can secure the most advantageous terms. Utilize the resources available through Mortgage Calculator to evaluate your financing options. Whether you're a first-time buyer, looking to refinance, or interested in investment opportunities, understanding the factors that influence mortgage rates can guide you in locking in a favorable interest rate and optimizing your home financing strategy.

What factors influence current mortgage rates?

Current mortgage rates are influenced by a variety of factors including economic conditions, the Federal Reserve's monetary policy, inflation, and your personal credit score. Understanding these elements can help you predict rate movements and secure favorable terms.

How can I compare different types of mortgage rates?

To compare different types of mortgage rates, you should look at the rates offered for 30-year fixed, 15-year fixed, FHA, VA, and Jumbo loans. Tools like the Mortgage Payment Calculator can assist you in comparing these rates and estimating your monthly payments.

Why is monitoring mortgage rate trends important?

Monitoring mortgage rate trends is essential because even small changes in rates can impact your monthly payments significantly. Staying informed about these trends allows you to capitalize on lower rates when they are available, optimizing your borrowing strategy.

How does my credit score affect the mortgage rates I'm offered?

Your credit score is a crucial factor in determining the mortgage rates you're offered. A higher credit score generally leads to more favorable rates, as it indicates lower risk to lenders. Conversely, a lower score can result in higher borrowing costs.

How can I improve my home affordability when considering a mortgage?

Improving home affordability involves strategic planning, including increasing your down payment and enhancing your credit score. Utilizing tools like Mortgage Payment Calculator to compare rates and forecast future rate movements can also significantly bolster your home financing strategy.