Home Equity Loan Calculator

Welcome to MortgagePaymentCalculator.io's Home Equity Loan Calculator, your trusted resource for estimating your home loan payments efficiently. Use this precision tool to analyze your available home equity, calculate potential borrowing amounts, and forecast your monthly payments based on your home's value, loan-to-value ratio, remaining mortgage balance, interest rates, and loan term. Whether you're planning home improvements, consolidating debt, or considering major expenses, this calculator empowers you with critical insights to guide your financial decisions confidently. Explore how leveraging your home's equity can align with your financial goals today.

Estimate your monthly payment, total interest, and repayment schedule.

Estimated monthly payment: $1,433.48

Based on a 15-year term at 8.00% APR

Principal vs. Interest

Payment interpretation

Borrowing $150,000.00 at 8.00% for 15 years produces an estimated monthly principal-and-interest payment of $1,433.48. Over the full term, you would pay approximately $108,026.06 in interest.

Home Equity Loan Repayment Analysis

Annual balance, cumulative interest, and cumulative payments.

Annual Amortization Schedule

See how much principal and interest you pay each year.

How Much Home Equity Can You Borrow?

Estimate borrowing capacity from your home value, mortgage balance, and lender LTV limit.

Estimated maximum home equity loan

Based on the selected combined LTV limit

At the selected LTV limit, the maximum combined debt secured by the property is approximately $480,000.00. After subtracting the current mortgage balance, the estimated amount available is $230,000.00.

Brief Overview

The Home Equity Loan Calculator at MortgagePaymentCalculator.io empowers homeowners by offering precise estimates of borrowing capacities based on home value, remaining mortgage balance, interest rates, and loan terms. This tool aids financial planning by providing insights into potential monthly payments and loan costs, crucial for informed decision-making on home improvements, debt consolidation, or major purchases. By understanding how variables like the loan-to-value ratio impact borrowing power, users can confidently align a home equity loan with their financial goals. Start using it today for a clearer picture of your financial capabilities.

Key Highlights

- Use MortgagePaymentCalculator.io's Home Equity Loan Calculator to assess borrowing power and monthly payments.

- Home equity is calculated as the difference between your home’s market value and outstanding mortgage balance.

- LTV ratio impacts loan eligibility and interest rates, with lower LTV favoring borrowing power.

- Accurate input in the calculator helps compare different loan scenarios for informed financial decisions.

- Aligning home equity loans with financial goals is essential for managing debt and achieving objectives.

Understanding Your Home Equity

Understanding your home equity is crucial for making informed financial decisions about leveraging your property's value. The more equity you have, the more options you gain for a home equity loan. Our home equity loan calculator will help you evaluate how much you'll pay towards your home equity loan, ensuring you maximize available funds. Home equity is the difference between your home's market value and any outstanding mortgage balances. By using the home equity loan calculator, you can determine potential loan amounts and align your home equity loan with your financial goals. Remember, each home equity loan can vary based on factors like interest rates, available equity, and your specific needs. Calculating your home equity is not only about knowing your home's value but also understanding how much you'll pay towards your home equity loan monthly. Use the home equity loan calculator to view different scenarios, helping you choose a home equity loan that fits your obligations. Ultimately, your home equity loan should support significant financial choices, from home improvements to debt consolidation.

What is Home Equity and How Is It Calculated?

Home equity represents the portion of your property that you truly own - essentially, the difference between your home's current market value and the amount remaining on your mortgage principal. To calculate your home equity, start by determining your home's appraised value, then subtract the outstanding mortgage principal. The result is your home equity, a key consideration when planning to use it for financial tools such as home equity loans. Interest rates, repayment periods, and the account type will influence your decisions, making it crucial to assess your needs. A careful evaluation of your account balance and the interest rate on potential home equity loans is vital for strategic planning. By understanding these factors, you can maximize your borrowing power. Having a grasp on how to accurately determine home equity empowers you to make informed decisions regarding interest rates, loan terms, and repayment strategies. Keep in mind that the interest rate and principal will directly impact the overall cost and monthly payment associated with utilizing your home equity effectively in your financial plans.

To make the most out of your home equity, consider these practical steps:

- Understand Home Equity: Calculate your home equity by subtracting any outstanding loan balances from the current market value of your home. Familiarize yourself with how it works to see how it can benefit your financial goals.

- Assess Your Financial Goals: Clearly define what you want to achieve by using your home equity, whether it's financing a renovation, consolidating debt, or investing. Align your decision with long-term plans.

- Research Financing Options: Explore various options like home equity loans, lines of credit (HELOCs), or cash-out refinancing to see which one best suits your needs and offers favorable terms.

- Consider the Costs: Be aware of fees, interest rates, and repayment terms associated with leveraging home equity. Calculate the total cost and ensure it doesn't outweigh the benefits you seek.

- Consult a Financial Advisor: Seek professional guidance to evaluate how tapping into your home's equity fits within your overall financial plan and whether it aligns with your risk tolerance.

- Improve Your Home's Value: If you use equity for home improvements, prioritize projects with high return on investment to increase your home value and potentially build more equity.

- Monitor Real Estate Market Conditions: Stay updated on housing market trends to time the usage of your home equity optimally, maximizing your financial returns.

- Maintain Financial Discipline: Use borrowed equity responsibly and avoid over-leveraging, which can put your home at risk if you're unable to meet repayment obligations.

These tips should help you make informed choices and utilize your home equity wisely for financial advantage.

Factors That Influence Your Home's Equity Value

Home equity can fluctuate due to several key factors, directly impacting your borrowing capacity when considering a home equity loan. The primary influencer is your home's value. As the market appreciates, your equity potentially increases, affecting loan opportunities. Another crucial element is the outstanding mortgage balance; as you pay down your mortgage, your home equity rises. Loan-to-value (LTV) ratios also play a significant role; a lower LTV can boost your borrowing power for home equity loans. Home improvements are another critical factor, potentially adding significant value, thereby enhancing home equity. Fluctuations in local real estate markets can also impact your home’s equity value, as changes in neighborhood desirability influence home prices. Economic conditions further shape interest rates on loans, which affect home equity borrowing strategies. Understanding these factors can help in leveraging home equity for financial goals, like debt consolidation or major purchases. With a well-informed approach, you can maximize your home equity loan potential while ensuring favorable loan terms.

Estimating Your Home Equity Loan Amount

Estimating your equity loan amount is crucial for making informed financial decisions. By analyzing your current mortgage balance and the available equity in your home, you can understand your borrowing options. The loan term influences your equity loan options and affects both your monthly payment and the loan amount you're eligible for. With the help of our calculator, you can estimate the impact different interest rate scenarios have on your loan amount and loan term. Choosing the right loan options requires considering the current mortgage rate and how it aligns with your financial goals.

Your account with MortgagePaymentCalculator.io can help you explore various equity loan options and ensure that the selected loan term suits your needs. By adjusting the interest rate in the calculator, homeowners can see how changes in economic conditions might affect their monthly mortgage commitment. It's vital to account for all these elements to ensure that the chosen equity loan supports your financial commitments and growth goals. This thorough approach can guide borrowers toward the most advantageous loan scenario.

| Key Factors | Tools & Resources | Loan Impacts | Strategic Considerations |

|---|---|---|---|

| Home Value | Appraisal Services | Determines maximum loan amount | Monitor market trends to leverage value appreciation |

| Existing Mortgage Balance | Mortgage Statements | Affects available equity for borrowing | Consider refinancing to potentially lower balance |

| Interest Rates | Rate Comparison Websites | Influences total cost of borrowing | Lock in lower rates to reduce long-term costs |

| Credit Score | Credit Monitoring Tools | Impacts interest rates and loan approvals | Improve credit score to access better loan terms |

| Debt-to-Income Ratio | Financial Calculators | Determines loan eligibility | Manage debts to maintain favorable ratios |

This table provides a streamlined overview of the critical components involved in home equity loan estimation and their implications for financial planning.

How to Calculate Your Maximum Loan Amount

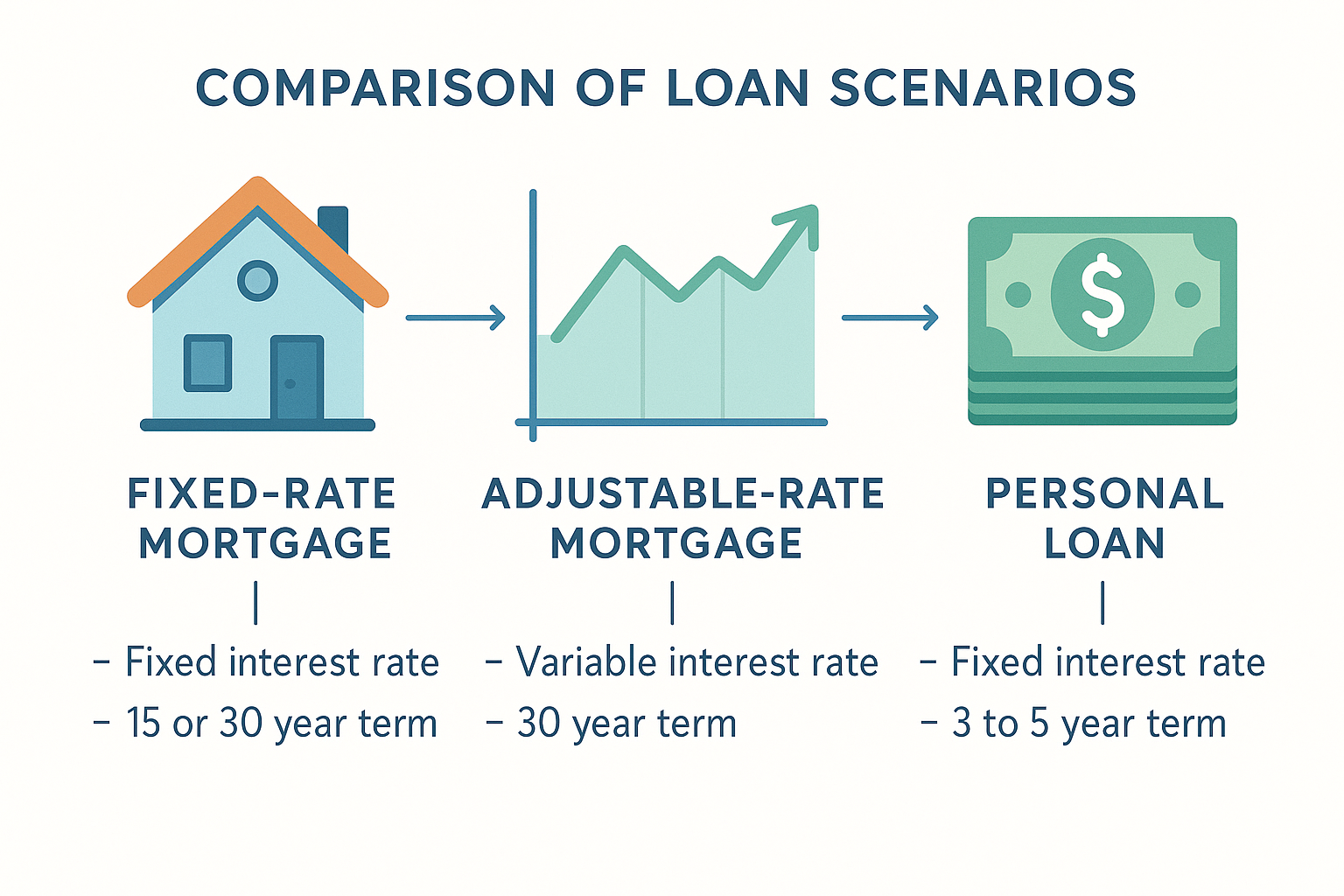

Calculating your maximum loan amount is a key step in making informed financial decisions. Start by assessing your current mortgage and personal financial situation. Your loan amount depends on your home's value, remaining mortgage balance, and available equity. Consider different loan term options to find what best suits your needs. The loan term impacts your monthly payments and overall interest rates. Use a reliable personal mortgage tool, like MortgagePaymentCalculator.io, to input your loan amount and loan term options, considering rates you might qualify for. Understanding the implications of different rates and loan options helps determine what's financially achievable. Knowing your loan amount gives clarity on potential investments or consolidating debt. Explore rate scenarios and account for variables like adjustable or fixed-rate loans. When you’re aware of your potential loan amount, aligning it with personal goals can be strategic. Don’t forget to consider how long you plan to stay in your home, as this affects the loan term and rates. With these insights, you're better equipped to navigate your loan options confidently.

Impact of Loan-to-Value (LTV) Ratio on Borrowing Power

The Loan-to-Value (LTV) ratio is a crucial factor determining your borrowing power for an equity loan. The LTV ratio compares your outstanding mortgage balance to your home's current value, affecting your loan eligibility and principal amount. A lower LTV ratio can enhance your chances of securing a loan by demonstrating to banking institutions your financial stability. When using banking tools to estimate your home equity loan, consider how the LTV ratio impacts your potential rates and loan term. An LTV below 80% typically allows for more favorable mortgage rates and flexible terms. Understanding the LTV ratio is essential for mortgage planning and leveraging an equity loan to align with your financial goals. MortgagePaymentCalculator.io provides tools to assess how your LTV affects your financial strategy, helping to estimate your loan term and payments. By calculating the LTV ratio, you get a clearer picture of your borrowing potential, aiding in effectively managing your mortgage account and planning any refinancing opportunities.

Using the Home Equity Loan Calculator Effectively

When using the home equity loan calculator, focus on accurately inputting data to get a clear picture of your home equity loan potential. Begin by entering your home's current value and any remaining mortgage balance. The home equity loan calculator then determines your home equity loan options, helping you estimate your loan-to-value ratio, a key factor in your borrowing power. Our calculator allows you to adjust different loan terms and interest rates, providing insights into various equity loan scenarios. This feature helps in choosing the best loan for your needs, whether for home improvements, debt consolidation, or managing education expenses. As you explore your loan options, remember that understanding how interest each month affects total costs and monthly payment amounts can refine your financial planning. By evaluating different equity loan scenarios, you can make informed decisions about your loan and align it with your financial goals. Let the home equity loan calculator guide you through estimating your borrowing capacity and understanding potential monthly payment obligations.

How to Use This Calculator for Accurate Estimates

To make the most of the Home Equity Loan Calculator, follow these steps for accurate estimates. Begin by entering your home equity details, including the current value and the outstanding mortgage balance. Next, decide on your desired loan amount, keeping an eye on the maximum home equity loan limits. Use this calculator to input the interest rate, predictability factors, and preferred repayment terms. The calculator helps visualize how your monthly payment varies with different loan amounts and repayment periods. Consider that the calculator also provides insights into the home equity line by calculating interest each month, enabling you to manage your financial commitments better. Look at the credit (HELOC) calculator features to compare against other financial products. Focus on the predictability of your monthly payment and repayment strategies to align with your financial objectives. Use this calculator frequently to reassess your options and ensure your home equity loan fits within your financial plan. Rely on the calculator to make well-informed loan decisions and optimize your borrowing potential.

Comparing Different Loan Scenarios

When considering a home equity loan, it's crucial to compare different loan scenarios to find the best fit for your financial needs. By using our Home Equity Loan Calculator, you can input various amounts and adjust the loan amount, interest rates, and repayment terms. For each loan scenario, the calculator will estimate your monthly payment, helping you account for future retirement, major home improvements, or emergency expenses. It's important to consider how different loan scenarios align with your financial objectives. Carefully evaluate your current home equity, required monthly payment, and the total loan amount to ensure it meets your budget and long-term goals. Keep in mind how different interest rates affect the overall cost of the loan. Before making any decisions, take into account your existing loans and other debts to maintain a healthy financial balance. Planning with precision will empower you to make informed choices about your equity loan, ensuring your financial well-being is protected over time.

Loan Repayment and Amortization Considerations

When evaluating a home equity loan, understanding loan repayment and amortization is crucial. Knowing how the principal paid changes over time can help you plan a predictable repayment schedule. With a fixed interest rate, your monthly payment remains consistent. The calculator estimates how your loan amount, interest rate, and term affect your monthly payment and principal. Initially, a more significant portion of your monthly payment covers interest, but over time, the principal paid increases. It's important to analyze how different loan amount scenarios influence your monthly payment. Whether you're dealing with a bank or another personal loan provider, understanding the intricacies of amortization can affect your financial decisions. Consider how your home equity loan aligns with your financial objectives. A well-planned loan amount and repayment strategy can maximize benefits while minimizing risk. By using the calculator, you can estimate the principal paid over time and ensure your home equity loan fits your budget.

Understanding Amortization and Interest Rates

In the realm of home loans, understanding amortization and interest rates is crucial. Amortization refers to how loans are structured, often involving fixed rate payments that blend both equity and interest. By comprehending this structure, homeowners can better anticipate their monthly payments on banking products like home equity loans. Loans are often influenced by the equity rate, with lenders considering your home equity and amortization terms to determine personalized rates. It’s important to consider the rate carefully, as it affects the overall cost of loans, including closing costs. Lenders offer various rates, so it’s essential to compare loans to find the best possible terms. Fixed rate loans provide stability, making it easier to budget as you repay through amortization. Closing costs should also be factored into the total cost of loans. As banking institutions have different equity evaluations, understanding your home’s equity can lead to more favorable terms. By mastering these concepts, you can make informed decisions and maximize your home equity loan benefits and goals.

Planning Financial Goals with an Equity Loan

Utilizing an equity loan can be a critical step in planning your financial goals. Whether you're aiming for retirement, tackling personal expenses, or managing fixed-rate obligations, strategically applying an equity loan can offer significant benefits. These loans provide a fixed installment plan that allows you to understand your financial commitments. With predictable interest each month, budgeting becomes more manageable. A critical part of this planning involves evaluating the loan amount and how it aligns with your needs. Our equity loan, specifically tailored for personal requirements such as paying off personal debts or financing major purchases, ensures you optimize the available equity. By leveraging tools like the credit (HELOC) calculator, you can estimate your monthly payment and assess how the fixed rate will impact your financial situation. It's essential to understand the account structure to maximize the benefits of your equity loan. Remember, the required payments depend on the chosen loan amount and the corresponding terms, making well-informed decisions crucial for successful financial planning.

Aligning Your Home Equity Loan with Financial Objectives

Considering a home equity loan can be a strategic decision to align with your financial objectives. When you seek predictable repayment schedules, the fixed rate of a home equity loan offers stability, allowing you to anticipate your interest each month without fluctuations. If you’re contemplating options for retirement or substantial purchases, knowing your home equity value is essential. The equity loan's ability to consolidate debt offers leverage in managing financial liabilities. A home equity line, or HELOC, can provide flexibility, but a structured repayment schedule through a loan might be more suitable for consistent budgeting. Using a home equity loan, you're capitalizing on your existing home equity, allowing you to explore options like home improvements or managing education expenses more effectively. By understanding your maximum borrowing capacity using a credit (HELOC) calculator, you can strategize appropriately. Loan-to-value ratios seriously impact your equity loan limits, guiding whether fixed terms align with your goals. It’s crucial to explore all loan options to fully integrate your home equity lending within your long-term financial planning.

Utilizing our Home Equity Loan Calculator at MortgagePaymentCalculator.io can empower you with the insights needed to make informed financial decisions. Whether you're planning home improvements, managing debt consolidation, or preparing for major purchases, our tool provides a clear picture of your borrowing capacity, estimated monthly payments, and overall loan costs. By understanding how factors like loan-to-value, interest rates, and remaining mortgage balance affect your financial strategy, you can better assess if a home equity loan aligns with your goals. Start calculating today to take charge of your financial future with confidence and clarity.

Frequently asked questions

What is home equity and how is it calculated?

Home equity is the difference between your home's market value and the outstanding mortgage balance. To calculate it, subtract the remaining mortgage principal from your home's current appraised value.

How does the Loan-to-Value (LTV) ratio affect my borrowing power?

The Loan-to-Value (LTV) ratio compares your remaining mortgage balance to your home's value. A lower LTV ratio can enhance loan eligibility and offer more favorable interest rates, increasing your borrowing power.

How can MortgagePaymentCalculator.io's Home Equity Loan Calculator help me?

The calculator helps estimate your borrowing capacity, monthly payments, and total loan costs based on your home's value, current mortgage, interest rate, and loan terms, assisting in informed financial decisions.

What should I consider when choosing a home equity loan?

Consider factors such as loan amount, interest rate, loan term, and how these align with your financial goals. Also, evaluate your current mortgage situation and how the new loan impacts your finances.

Why is accurate input important in the Home Equity Loan Calculator?

Accurate input ensures precise estimates of loan amounts and monthly payments, aiding in comparing different loan scenarios and making informed financial decisions.